Long Consumer Wellness

Exploring the Defining Consumer Driver of the Next Quarter Century

I have never been more confident in the long-term potential of the consumer wellness industry. If the first quarter of the 21st century was defined by the rise of e-commerce, the next quarter is shaping up to be all about health and wellness. We’re still in the early innings of what I believe is a generational investment opportunity.

The global wellness economy is already massive: McKinsey estimates it at $1.8 trillion, while the Global Wellness Institute puts it at $6.3 trillion — a 25% increase since 2019. Regardless of the source, these are needle-moving numbers within a much larger context: global consumer spending totals $61 trillion, with $16 trillion of that in the U.S. alone. For comparison, enterprise software — one of the highest-growth categories in tech — generates between $250 billion and $350 billion annually.

So the logical question is why now? This is a big market that has rather quickly gotten bigger recently — why won’t the law of large numbers start to slow this thing down?

It begins with a period of dislocation that’s still unfolding: GLP-1s have exploded into mainstream awareness, chronic disease has become a central issue in federal politics, and large CPG companies are reporting consistent volume declines despite an inflationary environment. Layered on top of this is a perfect storm of demographic and cultural shifts — younger consumers are prioritizing wellness more than any generation before them, and a growing focus on longevity is pushing health to the center of mainstream culture.

Dislocations

It’s been less than four years since GLP-1 agonists (“GLP-1s”) like Ozempic and Wegovy began being prescribed in the U.S. for obesity, yet the market has already reached staggering scale. U.S. sales of GLP-1s totaled $13 billion in 2024, with 2% of the population currently on the drug — and 9% expected by 2030. If this trend continues, we may be approaching the peak of obesity rates in the U.S. In 2023, the national obesity rate declined slightly from 44.1% to 43.9% — the first drop in over a decade.

Whatever the trendline, obesity rates remain far too high — and a long-overdue sense of alarm is finally entering the cultural conversation. The statistics are staggering: 6 in 10 American adults have at least one chronic disease; 4 in 10 have at least two. Nearly half of Americans suffer from heart disease. 11% have diabetes, and another 38% are pre-diabetic. These numbers point to several uncomfortable truths: we have a severe population-wide health crisis; government policy has often exacerbated the problem (through subsidies and flawed nutritional guidance); and the economic impact is immense — 90% of the U.S.’s $4.5 trillion in annual healthcare spending goes toward treating chronic disease.

Public awareness of the chronic disease crisis surged in 2024, driven in part by the sibling duo Dr. Casey and Calley Means. Through appearances on prominent podcasts and growing influence within the RFK Jr. and later Donald Trump presidential campaigns, they helped elevate chronic disease into a national political issue. Their “Make America Healthy Again” (MAHA) platform emerged as a defining movement in the 2024 election cycle. The conversation about organic ingredients, ultraprocessed foods and environmental toxins can no longer be dismissed as “coastal”.

This cultural reckoning — combined with the widespread adoption of appetite-suppressing drugs — has become a significant headwind for manufacturers of empty calories. Big CPG companies are expected to grow through all parts of the economic cycle without margin compression (and their stock valuations reflect that), but that growth is beginning to look increasingly unsustainable.

Since 2022, during a period of sustained inflation, large-cap CPG players have leaned heavily on price increases to offset stagnant or declining volumes. According to Bain, 95% of 2023 CPG growth in North America came from pricing rather than unit growth.

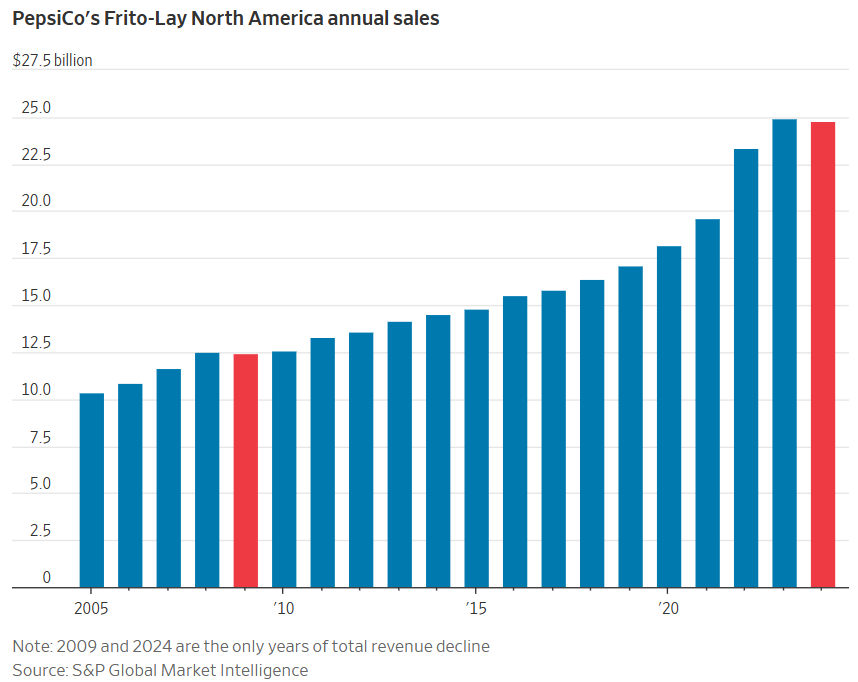

The pricing lever is tapped out and even the most entrenched monopolies are feeling the strain: in 2023, Frito-Lay reported its first annual sales decline since the global financial crisis. If legacy CPG companies can no longer grow organically, they face an identity crisis. Their only option may be to finally give consumers what they want: healthier products.

The problem? What consumers want isn’t in their brand or product portfolios today.

Catalysts

Dislocation creates opportunity. In 2025, consumers are operating with radically different information about their health than they had just a decade ago. We've seen a sharp reversal of outdated nutritional beliefs (remember ‘low fat’?), a global pandemic that disproportionately affected those with chronic conditions, and the near-universal adoption of wearables delivering constant streams of personal health data.

As a result, consumers are taking far greater control of their well-being. For many, it has become their top priority. Forerunner’s 2025 Annual Trend Report highlighted Health & Wellness as the number one life goal for consumers — ranking even higher than family, friends, or finances.

This rising interest has triggered a paradigm shift. Consumers are rebuilding their understanding of health from first principles. As trust in traditional institutions has eroded, a new group of voices has stepped in to fill the gap: we call them the Longevity Leaders.

Andrew Huberman, Peter Attia, and Bryan Johnson have become the go-to authorities on health, wellness, and longevity.

– Andrew Huberman is a neuroscientist and professor at Stanford School of Medicine, best known for Huberman Lab, one of the world’s top-ranked science podcasts, with millions of monthly listeners across YouTube and Spotify.

– Peter Attia is a physician focused on longevity and performance, and the bestselling author of Outlive, which topped The New York Times list and helped cement his influence through his podcast The Drive and a growing subscriber base.

– Bryan Johnson is a tech entrepreneur and biohacker, known for founding Kernel and Braintree. He’s now recognized for his radical anti-aging experiment Blueprint, which became the subject of a widely viewed Netflix documentary exploring the future of human healthspan.

Together, these three have become cultural arbiters of how to live healthier, longer lives. For any topic — from strength training to alcohol consumption to sleep — the default question has become: “What do Huberman, Attia, or Johnson say about it?” It's no surprise we've seen an explosion in protein consumption, a collapse in alcohol consumption, and booming success stories from sleep optimization brands like Oura and Eight Sleep.

The Opportunity

So to summarize, we have:

A chronic disease crisis

A generational weight loss drug

A volume decline in one of the world’s largest and most recession-proof industries

Health and wellness becoming the top life priority for consumers — even above family and friends

A complete reshaping of authority within the health and wellness ecosystem

All within a global market that is already enormous: over $6 trillion in size — roughly 20x the scale of enterprise software.

Fast-forward twenty-five years, and the shelves at Walmart and Target — along with the brand portfolios of Unilever and P&G — will look dramatically different. They’ll be far more aligned with what consumers truly want. The devices and services people use to monitor and manage their health will be vastly more advanced. And our collective understanding of how to live better, longer lives will have grown exponentially. This is set to be a defining quarter-century.

Long dismissed as trend-driven, the consumer economy now has a new anchor: truth. People want to understand, engage with, and improve their health — and they’re willing to spend more than ever to do it. For the companies and investors operating in this space, the opportunity is generational.

I am long consumer wellness — and I believe this is only the beginning.

Great article !

Well said